Sophisticated investors are keenly aware of the benefits of diversification. By spreading your investment across different asset classes and industries, you are less likely to experience shocks that impact your entire portfolio the same way. In an environment where traditional portfolio diversification methods no longer offer the same durability, investors are increasingly turning to alternative assets to mitigate against risks. Mortgage Investment Corporations, or MICs, offer significant diversification benefits when compared to traditional assets like stocks and bonds.

Mortgage Investment Corporations are investment portfolios that pool capital from investors to lend borrowers in the form of first and second mortgages. Investors who deposit money into a MIC become preferred shareholders in the fund, creating an alternative fixed-income investment that entitles them to regular dividends – typically monthly – in the form of fees and interest paid by the borrowers. Because MICs are not bound by many of the same lending requirements as traditional banks, they can set their own criteria for adjudicating and approving loans. In practice, this gives MICs the ability to charge higher interest rates on mortgages than traditional banks.

Investors are choosing to invest in MICs because they have historically provided higher rates of return than traditional fixed-income securities like government bonds. MICs are classified as “flow-through” investment vehicles under the Income Tax Act, which means they can avoid paying taxes by distributing 100% of their net income to shareholders. MICs can also be incorporated into a Tax-Free Savings Account (TFSA) and Registered Retirement Savings Account (RRSP), giving investors more flexibility in growing their portfolio without immediate tax implications.

“60/40 Portfolio” Is No Longer a Guidepost

Since at least 1929, the “60/40 portfolio” has been a guidepost for the moderate risk investor. By allocating 60% of their portfolio to stocks and 40% to bonds, investors were able to enjoy capital appreciation and predictable yield in a single portfolio. But what happens when bonds don’t go up when stocks go down and vice versa? As it turns out, inflation poses a major challenge to the traditional 60/40 portfolio – bonds may be a reliable diversifier in periods of slower economic growth but not necessarily when inflation is rising. Inflation has risen to four-decade highs across most developed economies. While central banks have responded by raising interest rates aggressively, their ability to cool inflation without triggering recession is still under scrutiny. As investors rethink the diversifying nature of stocks and bonds, they’ve also recalibrated their portfolios, opening the door to alternative investments like MICs.

According to Manulife Investment Management, Canadian pension plans with over $500 million in assets already allocate 35% of their portfolios to alternatives. In the United States, state and local government pension plans increased their allocation to alternatives from 9% in 2001 to 34% in 2022. How much an individual investor chooses to allocate to alternatives will depend on their underlying objectives and whether their investment decisions are driven by capital preservation, fixed-income diversification, inflation hedging, or some other goal.

For individual investors, MICs provide additional diversification benefits through exposure to Canada’s diverse mortgage market and, by extension, Canadian real estate.

How MICs are Diversified

While investing in MICs is a diversification strategy of its own, leading MIC funds benefit from geographic diversification, or the process of investing in mortgages across various geographic regions. Geographic diversification is especially important during periods of uneven demand for residential loans due to changes in monetary policy or the economy. Even during relatively stable periods, Canada’s geography, population and economy vary significantly across the country, making geographic diversification an important anchor of a well-managed MIC.

Even with the recent softening of the housing market due to rising interest rates, home prices in places like Calgary, Regina, Saskatoon and St. John’s are barely off their peaks, according to the Canadian Real Estate Association (CREA). By comparison, parts of Ontario and British Columbia – historically home to the strongest housing markets in terms of sales, price growth and inventory levels – have experienced larger corrections over the past year.

A geographically diversified MIC has exposure to many of these markets, mitigating the risk of over-concentration in one jurisdiction. The most successful MIC funds have a strong presence in major cities like Toronto or Vancouver but also invest outside of these regions where competition is lower and the potential for higher yields is greater. Some of the most attractive mortgage markets exist in smaller cities due to heightened demand for alternative lenders and lower service coverage than in major cities.

In addition to geographic diversification, MICs are diversified by borrower type, mortgage type, loan duration and loan-to-value ratios. All loans approved by the MIC are assessed for credit risk, transaction type and the borrower’s ability to repay. However, beyond the necessary due diligence process, MIC funds can be constructed to meet certain performance targets. Well-managed MIC funds offer investment opportunities that match various risk profiles and investment horizons – from conservative to balanced and up to high yield.

The CMI Difference

CMI Financial Group has become one of Canada’s fastest-growing non-bank financial institutions by focusing exclusively on private mortgage lending and investments. With nearly $2 billion in successful mortgage placements, CMI offers investment portfolios that suit the needs of investors of various risk profiles. As a lender in both urban and rural housing markets across Canada, geographic diversification allows CMI to build mortgage portfolios from a broadly curated portfolio of loans.

CMI MIC Funds offers three district mortgage funds with yield targets tied to specific risk and return profiles.

The CMI MIC Prime Mortgage Fund is a more conservative fund designed to minimize volatility by investing primarily in first mortgages with an average maximum loan-to-value (LTV) of 65%. The fund aims to deliver targeted annual returns of 6% to 7%.

The CMI MIC Balanced Mortgage Fund targets higher annual returns of 8% to 9% by investing in both first and second mortgages and by increasing the average maximum LTV to 75%.

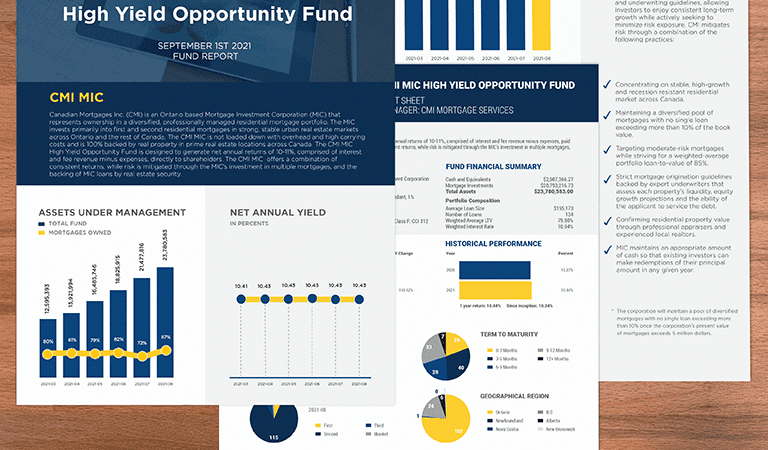

The CMI MIC High Yield Opportunity Fund aims to deliver targeted annual returns of 10% to 11% by investing primarily in second mortgages with an average maximum LTV of 85%. Compare CMI MIC Funds.

CMI Financial Group gives investors access to all the diversification benefits Canada’s mortgage market has to offer. Interested in learning more about how to become a private lender? Contact us now to learn more about our investment process or to request a free consultation with one of our investment professionals.