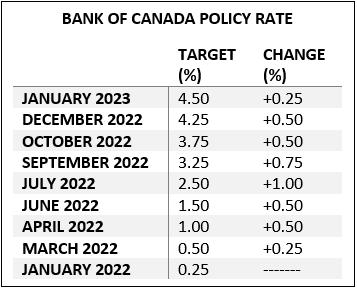

- At its January 25th meeting, the Bank of Canada (BoC) raised its policy rate to 4.5%, an increase of 4.25 percentage points since January 2022.

- The BoC will continue with Quantitative Tightening (QT) by removing liquidity from the financial system. Since it began QT, the BoC has reduced the size of its balance sheet by about $165 billion and, in 2023, we expect another $88 billion in liquidity to be removed as the BoC lets its bond holdings run off.

- The BoC Monetary Policy Report – January 2023 sees “growing evidence that restrictive monetary policy is slowing activity, especially household spending.”

Key Takeaways

Policy Lags – The full effect of interest rate increases will take between 18 and 24 months, as higher rates affect discretionary spending plus interest sensitive expenditures such as homes, vehicles, and large durable purchases.

3% Inflation – The BoC expects inflation to be 3% by the middle of 2023. The annual inflation rate is calculated as the percentage change since the same month in the previous year and, since most of the price increases happened between January and March of 2022, the BoC expects the inflation rate to be 3% by mid-2023. Recent work by Trevor Thom and Sonja Chen indicates that global supply-side factors for food and fuel were major contributors to Canada’s inflation. In the last year, food prices have fallen more than 13%, and oil is down over 30% from the highs of last summer.

Housing and Mortgage Markets – The move in rates increased the number of variable rate borrowers who now have hit their trigger rates (estimated to be 73% by National Bank Financial). While the BoC and most analysts are expecting house prices to fall further, housing activity should pick up in the second half of 2023, given low inventories and strong demand from immigration.

What to Watch

Core Inflation – The Bank focuses on two measures of inflation, CPI-trim and CPI-median, that remove extreme price volatility. Declines in these metrics will be a pre-condition for the BoC to lower rates.

Labour Market – Employment growth moderated in the second half of 2022, especially in sectors sensitive to interest rates, but labour markets remain tight. An easing in the labour market will give the BoC more impetus to lower rates.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any person or organization in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice including investment advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication. Readers are cautioned to always seek independent professional advice from a qualified professional before making any investment decisions.